Start a Business Credit Profile and Bring the Business Credit Mountain Down to Size

There once was a man. His name was Joe Entrepreneur. Joe had huge, amazing ideas. He worked hard to turn those idea into reality, but there was a challenge. He couldn’t go around, under, or through it. It was the business credit mountain, and Joe knew he had to go over it. Not one to make things harder than they have to be, he began looking for ways to make a molehill out of the credit mountain, and he succeeded. What did he learn? We have all the secrets. The first step was to start a business credit profile.

This is the first step, but there are many steps needed just to get to the base of the mountain. He is still miles away, and he has to actually start walking to get there. Once you start a business credit profile, you are at the base, and you can start bringing the top down to you. So how do you get to the base? Read carefully as we share the 3 essential steps that will take you straight there.

Why Business Credit?

You may be wondering why this mountain is there in the first place. Why does Joe have to climb up it to turn his brilliant business ideas into reality? Why can’t he just use his personal credit score? Also, why do so many start the climb only to fall back down to the bottom?

You may be wondering why this mountain is there in the first place. Why does Joe have to climb up it to turn his brilliant business ideas into reality? Why can’t he just use his personal credit score? Also, why do so many start the climb only to fall back down to the bottom?

If you have great personal credit, you can definitely use to get started. Joe knows this isn’t always wise however. Just because you can, doesn’t mean you should. There are a couple of reasons for this.

First, business credit usually has higher limits. This is necessary when it comes to funding a business. Large cash outlays are required in the daily operations of most any business, and that can max out personal credit limits quickly.

Another reason to build your business using business credit rather than personal credit is protection. If your business is tied to your personal credit, then it can affect your personal credit both ways. If your business goes south, your personal credit will tank.

Even if your business is booming, it can still have a negative effect on your personal credit. Those lower limits on personal credit will get maxed out quickly, as Joe already knows. That lowers the debt-to-credit ratio. That ratio is a factor in your personal credit score, and if it is too high, it has a negative impact.

So, even if you are making payments on time, business accounts being reported on your personal credit report could cause problems.

The Benefits

When your business it built on its own credit, you don’t have to worry about it affecting your personal credit. Not only that, but if your personal credit isn’t the best, your business can still grow and thrive as long as it has its own strong credit score. Thus we come to the reason for Joe’s impending climb up the business credit ladder.

What is a Business Credit Profile?

This is your file with the business credit bureaus. If your business does not have a business credit profile, then it has no credit score. When a lender tries to check a business credit score and there is no business credit profile, it comes back as “no credit.” In a lender’s eye, this is exactly the same as bad credit.

If a lender tried to report payment history on a business that does not have a business credit profile, it will simply go on the owner’s personal credit report.

You have to start a business credit profile, it doesn’t just appear. It is an intentional process that happens in multiple steps.

Step One: Bring the Mountain Down One Rock at the Time (Establish Your Business to Start a Business Credit Profile)

How do you bring down a mountain? One rock at a time. We have the equivalent of a bulldozer to help you out, but it all starts with that first rock. Your business credit profile is that first rock. To ensure your business credit profile and thus your business credit is on a solid foundation, you must establish your business as an entity separate from yourself.

On the surface, this may seem a little ridiculous. You might even be thinking “of course my business is separate from myself.” However, if your business only has a separate name, but shares your address, phone number, and bank account, in the eyes of credit agencies and lenders it is the same as you.

If this is the case, all of your business transactions are being reported on your personal credit, and there is no business credit profile. Check the following off your list to begin the process of establishing your business as a separate entity and start a business credit profile.

- Set up a separate address for your business. A virtual address will work, but it cannot be the same as your personal address.

- Obtain a dedicated phone number for your business from a toll-free exchange and list it in the directories under the business name.

- Create a professional looking website for your business. It does not have to be complicated, but it needs to be user friendly and professional. All links should work and it should be free of typos.

- Set up a dedicated email address specifically for the business. Stay away from free email accounts like yahoo and Gmail. It should be something related specifically to the business website.

- Incorporate your business

A Word about Incorporation

Incorporation is a vital step when separating your business from yourself legally. You do this through the IRS website. There are a few options for this. The option you should choose will depend upon what works best for your business and needs.

Corporation

This is the most expensive option, but it also offers the most protection from liability. There is a double taxation caveat with this option that is a turn off for most. Owners pay tax at both the business level and the shareholder level. In some cases, this is the best option anyway.

S-Corp

S-Corps are very similar to corporations, but double taxation isn’t an issue. There are also limits on the number of shareholders allowed among other restrictions set forth by the IRS.

LLC

An LLC, or a limited liability corporation, is the least expensive option. It still offers some liability protection and is has few restrictions than an S-corp.

Each of these options serves the purpose of further separating the business from the owner when you are looking to start a business credit profile. The option you choose should be the one that best suits your needs for tax purposes.

While you are on the IRS Website, you will also want to register for an EIN. This is the business equivalent of a social security number. If you use your SSN to apply for credit for your business, your personal credit will get involved. By using a unique identification number specifically for the business, you ensure that your business is separate from your SSN.

Step 2: Shore Up Loose Rocks (D-U-N-S #)

If Joe tried to to bring that mountain down without shoring up loose rocks, you will end up buried. The D-U-N-S number is a loose rock that needs to be taken care of before it knocks you in the head.

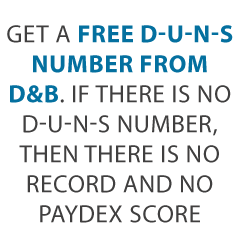

Dun & Bradstreet is the premier business credit agency. It is the largest and most used of the three, the other two being Equifax and Experian.

Before you can start a business credit profile with Dun & Bradstreet, you have to have a D-U-N-S number. You will have no profile with them if there is no D-U-N-S number associated with your business. It is free to get one on the Dun & Bradstreet website. They will try to sell you other services when you apply, but don’t them fool you. You do not need anything else, and the number itself is absolutely free.

Step 3: Move the First Shovel Full of Rock

It’s time to crank up that backhoe and start taking down that mountain by the shovel full. Sometimes this is the hardest step to take. In credit terms, it can seem almost impossible. That is because even if you have taken all the other steps and reached the bottom of the ladder, you cannot start a business credit profile without reported credit.

That’s right, you have to have credit to build credit. You must have credit accounts reporting before you can have a business credit score. I know, right now your head is spinning. It seems like an impossible situation because in most cases, you have to have credit to get credit. All lenders check your credit score, right?

If you don’t have business credit, how can you get credit for your business without a personal credit check?

The answer, that first shovel full of rock that seems to be the hardest to move, is the vendor credit tier. These are companies that will offer invoices with net 30 terms and report your on-time payments to the credit agencies.

To receive net terms on invoices with these companies, you may have to make a few purchases initially. Then, you can apply for net terms. Typically, they will want to see at least a minimum amount of time in business, anywhere from 6 months to 3 years, depending on the vendor.

3 Top Players in Starter Credit

There are a ton of vendors out there, but when you need to start a business credit profile, these three make a great starting point.

Grainger Industrial Supply

Grainger is a vendor that sells hardware, outdoor equipment, and even power tools. To apply for net terms, you will need and EIN as well as a D-U-N-S number. They accept applications via phone or fax. If you need more than $1,000 in credit, you will need bank and trade references, but if you need less than $1,000 you only need a business license.

Getting started, you will not likely have trade references. That’s okay, because less than $1,000 is fine to start a business credit profile. Simply apply, and when you get approval, order things you need for your business anyway and make the payment on time. Get started here. Read our full Grainger net 30 review here.

Marathon

Check out starter vendor Marathon. Marathon Petroleum Company provides transportation fuels, asphalt, and specialty products throughout the United States. Their comprehensive product line supports commercial, industrial, and retail operations.

This card reports to Dun & Bradstreet, Experian, and Equifax. Before applying for multiple accounts with WEX Fleet cards, make sure to have enough time in between applying so they don’t red-flag your account for fraud.

To qualify, you need:

• Entity in good standing with Secretary of State

• EIN number with IRS

• Business address- matching everywhere.

• D-U-N-S number

• Business License- if applicable

• A business Bank account

• Business phone number listed on 411

Your SSN is required for informational purposes. If concerned they will pull your personal credit talk to their credit department before applying. You can give a $500 deposit instead of using a personal guarantee, if in business less than a year. Apply online. Terms are Net 15.

Uline Shipping Supplies

Uline carries shipping boxes, janitorial supplies, and more. They report to D&B, so you have to have a DUNS number before you get credit terms with them. They will ask for a bank reference along with two other references. It may be necessary to prepay at first. Once you do that, they are likely to approve net 30 terms. Find out more about Uline here. You can also read our full Uline net 30 review.

Now What: Keep Moving Rocks

After you move the first shovelful, you no longer have to worry about how to start a business credit profile. Now you just have to focus on building a strong credit score. Before you know it, the top of that credit mountain will be right in front of you. What lies in store for Joe between that first rock and the goal?

There are a few more credit tiers to dig through. After the vendor credit tier comes the retail credit tier. These are credit cards offered by stores such as Best Buy, Costco, Office Depot, Amazon, and even Walmart.

If you make your payments on time to the vendors in the vendor credit tier, those reported payments will ensure your score is strong enough to be get approval for credit in the retail credit tier.

Next comes fleet credit. These are cards offered by companies such as Fuelman and Shell that you can use for fuel and vehicle maintenance and repair. Reported on-time payments to these creditors will build your credit even further.

Then you can apply for more universal credit. These are your traditional credit cards such as Visa, MasterCard, and American Express. Once you are here, you should be able to see the top of the mountain clearly.

Watch Out for Rock Slides

Joe knows that there is the potential to to stray rocks to break loose no matter how well he shores things up. No one wants to dodge rocks they can’t control. If you fail to make your payments consistently on-time however, this is just what will happen. The ground will give way and you could end up buried underneath.

It could take you a while to dig your way out and start moving rocks again.

The View Over the Top

What will Joe see when he gets the mountain down to size? The same thing you will when you can see over the top. The green grass really is greener on the other side. At the top of the business credit mountain is a world of funding opportunities. These include, among other things, traditional term loans and business lines-of-credit from traditional lenders.

Once you have the top down where you can reach it, you can access all the funding you would ever need to grow your business and ensure its success. It all begins when you initiate the journey to the foot of the mountain to start a business credit profile.